Juggling credit cards, personal loans, car finance and a mortgage is a reality for many Australians, often causing stress and a sense that there’s no clear way out.

Debt consolidation can help you regain control by simplifying repayments and reducing costs, but the right approach depends on the types of debt you hold and the assets you have behind them.

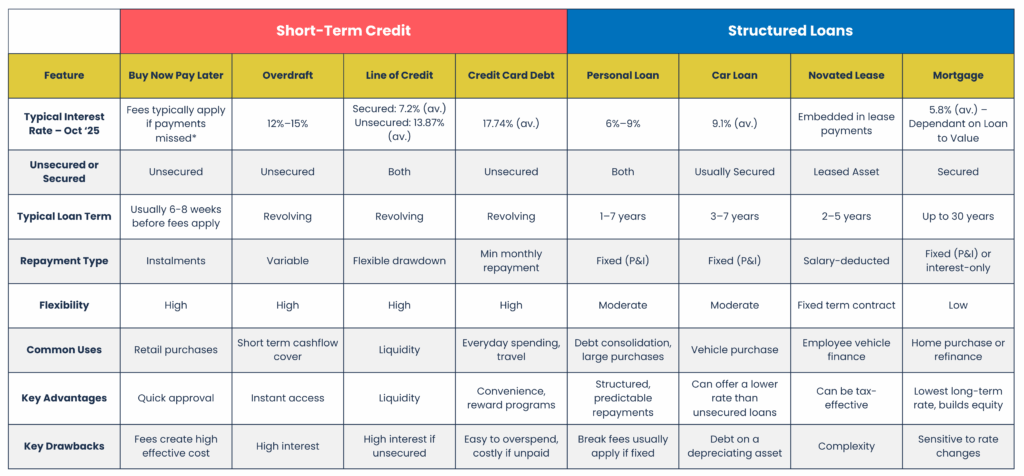

Before exploring your options, it helps to understand how Australia’s most common types of personal debt work.

Personal debt in Australia

Short-term debt tends to offer flexibility but at a higher cost, while long-term debt trades flexibility for lower interest rates. The table below outlines the key features of common types of debt in Australia.

*Can result in an effective annual rate exceeding credit card rates

What is debt consolidation and how does it work?

Debt consolidation is the process of combining multiple debts into a single new loan, ideally with a lower interest rate and structured repayment schedule. The goal is to make debt both cheaper and easier to manage within your overall budget.

Effective consolidation targets high-interest, non-deductible debts with flexible repayment terms, such as Buy Now Pay Later loans, credit cards, and overdrafts.

To provide certainty and structure, the new loan will typically be structured as a personal loan or a mortgage with a fixed term and often a fixed rate of interest.

Example – pay off credit card debt faster with lower-rate borrowing

This example shows how using lower-rate debt can shorten repayment time and reduce total cost without changing monthly repayments.

Suppose you have credit card debt of $10,000 accruing interest at 15% with repayments of $167 p.m. It would take around 112 months (c. 9 years) to clear the balance at a total cost of $18,599.

Now assume you have a mortgage with an interest rate of 5.5% and your lender allows you to establish a new loan tranche of $10,000. By using this to repay your credit card, while maintaining repayments of $167 p.m., it would take you 71 months (c. 6 years) to repay the debt, at a total cost of $11,721.

This approach works as more of your payments are directed to reducing the loan, rather than paying interest.

Potential drawbacks and when debt consolidation might cost you more

Consolidating debt provides structure that is often based on an extended loan term. While this can ease short-term pressure by reducing monthly repayments, it may increase the total interest cost over time.

Using the example above, if the $10,000 mortgage balance were repaid over 30 years, the monthly repayment would fall to $57, but the total cost would rise to $20,440.

The key to a successful debt-consolidation strategy is therefore to maintain or increase your existing repayment level, taking advantage of the lower rate without stretching the term.

Consolidating debt can also mean giving up flexibility and accepting early-repayment charges. If your financial position improves and you’re able to pay off debt faster, doing so may come with additional costs.

Finally, while converting unsecured debt into a home-secured loan reduces costs, it also puts your property at risk if repayments aren’t maintained.

Debt consolidation works best with a budget

For many people, juggling multiple debts stems from living beyond their means. In these cases, the first step towards financial stability is a clear budget.

Debt consolidation should form part of a broader budgeting plan designed to keep expenditure within income. Simplifying repayments and lowering interest costs can free up cash flow to clear debts faster.

Having consolidated your loans, maintaining discipline is essential. Some borrowers clear their credit cards with a consolidated loan, only to start using them again.

Once the credit is cleared, cut the cards and focus on building habits that keep you out of debt for good.

Start with reliable guidance

Free, impartial help is available from the National Debt Helpline (1800 007 007).

Before engaging an advice service, always check that the provider appears on ASIC’s Financial Advisers Register.

Meet Daniel at Dorset Wealth Management or Find a Planner near you!

The Money & Life website is operated by the Financial Advice Association Australia (FAAA). The views expressed in this article are those of the author and not those of the FAAA. The FAAA does not endorse or otherwise assume responsibility for any financial product advice which may be contained in the article. Nor does it endorse or assume responsibility for the information.